Summary

The Bangladesh Bank has recently introduced a new framework that aims to promote financial stability and maintain public confidence in the banking system. This framework categorizes troubled banks into four groups based on their non-performing loans (NPLs) and Capital to Risk (Weighted) Assets Ratio (CRAR).

Content:

As per the Prompt Corrective Action (PCA) Framework, if a bank’s Non-Performing Loans (NPLs) exceed 14% and their Capital to Risk-Weighted Assets Ratio (CRAR) falls below 5% for 24 consecutive months, they will be placed in Category 4. In such a scenario, the bank will not be allowed to accept any new deposits or extend new loans without prior approval from the central bank.

According to a circular issued by the central bank yesterday, banks that have a CRAR (Capital to Risk-Weighted Assets Ratio) of more than 10% and NPLs (Non-Performing Loans) remaining below 8% for six consecutive months will be classified as Category 1. These banks cannot pay cash dividends to their shareholders, but they may distribute stock dividends after obtaining the central bank’s prior approval. On the other hand, banks that have a capital ratio lower than 10% and non-performing loans exceeding 8% for twelve consecutive months will be placed under Category 2.

Banks falling under Category 3 have non-performing loans exceeding 11% and a capital ratio below 8%. These banks are not allowed to open new branches, sub-branches, or subsidiaries, either domestically or overseas, without the central bank’s consent. Moreover, they are prohibited from engaging in any new transactions with related parties without prior approval from the central bank. Their investment in existing subsidiaries, either domestically or overseas, is also restricted. Furthermore, banks falling under this category will be prohibited from distributing dividends to raise retained earnings. The growth rate for their operational costs is limited to 5% of the previous year’s expenses. Lastly, these banks are only permitted to engage in capital expenditures related to automation or technological development.

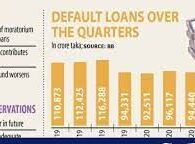

Based on their audited financial reports for 2024, banks will be classified and the new framework will become effective in May 2025. A crisis in the banking sector has been created by anonymous loans, a liquidity shortage, high non-performing loans (NPLs), and family influence in the appointment of directors, according to a central bank official. Furthermore, the lack of sound governance is impeding the proper functioning of banks. The International Monetary Fund (IMF) has instructed Bangladesh to carry out extensive policy reforms as part of the conditions for the $4.7 billion loan granted to the country. According to the circular, the Bangladesh Bank has the authority to remove any bank from the framework once it meets normal criteria and maintains that status for four consecutive quarters.

A managing director of a private bank emphasized that the banking sector is currently facing numerous crises. The sector is plagued by fictitious loans, liquidity shortages, high default rates, and nepotistic board appointments, which have led most banks to borrow capital to remain operational. Additionally, weak governance practices have hindered effective bank management. In a circular, the central bank has highlighted the importance of taking early action to prevent adverse and systemic effects of troubled banks on the banking system and the broader economy. The circular also emphasizes the need for prompt corrective action, as closing down a bank is an expensive and disruptive process. This is why the framework was introduced.

Picture and Article Sources: The Business Standard